On the sunny, chilly morning of January 20, 1981, as the country faced crippling double-digit inflation and a smoldering banking crisis, Ronald Reagan swore the oath to become the nation’s 40th president. “Government is not the solution to our problem, government is the problem,” he famously pronounced.

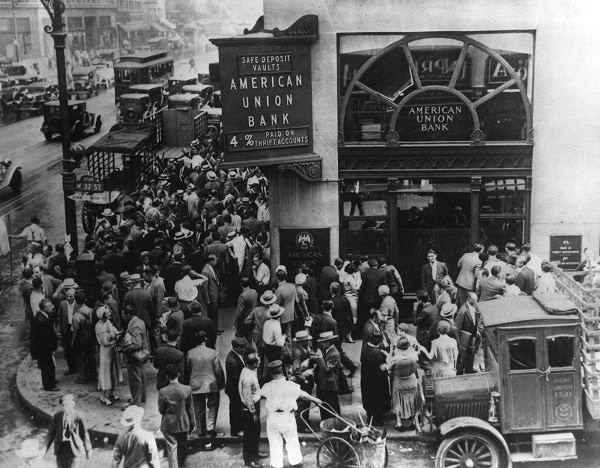

Congress established federal deposit insurance during the Great Depression, in part to stop the bank runs common in that period. Wikimedia Commons

Reagan was right, but not as he intended: over two terms, his White House, with the active participation of his vice president, George W. Bush, would hide the extent of the bank crisis from the American people, and, in the process, render what was initially a $50 billion problem into one that would cost 10 times more to fix. Reagan rode into office promising lower taxes and less government, but his administration’s poorly executed implementation of the latter led to the most expensive bailout in US financial history. The bailouts during the Great Recession in 2008 totaled in the trillions—$24 trillion by one reckoning—but because most was repaid or not used, the bailout during the 1980s bank crisis retains the title as most expensive for taxpayers.

At the heart of the 1980s crisis was federal deposit insurance, which the US Congress had enacted 50 years earlier during the Great Depression, despite initial objections from President Franklin Delano Roosevelt. It works like this: Banks pay an insurance premium into a federal fund that guarantees that, if a bank fails, depositors will receive their deposits up to a specified amount—when adopted in 1933 it was $2,500, today it is $250,000. If the premiums banks pay into the fund prove insufficient during a time of economic crisis, taxpayers must fill the gap.

Roosevelt agreed that deposit insurance would stop the bank runs plaguing the country but argued it also would create moral hazard in depositors, who, knowing their money was safe no matter what, would become indifferent to whether bank executives ran institutions safely or not. He proved to be correct. During the 1980s bank crisis, Reagan allowed hundreds of insolvent banks to remain open. The sicker these institutions became, the more incentive they had to find cash that they could invest in high-risk but potentially high-return ventures—and possibly grow out of their troubles. To raise this cash, the banks paid higher-than-market interest rates. Depositors, knowing they would be paid no matter how risky the banks’ behavior was, flocked to put money into them. The high-risk gambling failed, and banks became ever more insolvent.

Deposit insurance did not cause the initial crisis of the 1980s. Oil-price hikes that sent inflation soaring—as well as the deregulation of financial services that sent companies into businesses they didn’t understand—did that, pushing thousands of banks that specialized in mortgage lending into the red. These specialty banks, known as thrifts or savings and loans, made long-term loans—mortgages—that were good but not good enough. Home loans were yielding single-digit returns, but thrifts were paying double-digit interest on short-term deposits as a result of inflation. It was a classic interest rate squeeze.

The country had, as has been the case so often in its history, too many banks. The government should have shut these banks, used $50 billion in taxpayer funds to cover the shortfall that was owed to depositors, and moved on to other issues. Instead, the White House that preached free market economics kept the legion of dead banks alive with massive government subsidies and a green light to diversify out of mortgages and into just about anything else. The short-term goal was to maintain the fiction that these walking dead were fit. Elected officials hoped that at least some of these sick banks would grow out of their problem.

The tactic did not work, but no matter. The ultimate strategy was to postpone, until after Reagan and Bush won their collective three terms in office, any mention to the public of the need for tens of billions—and as time wore on, hundreds of billions—in taxpayer dollars. In 1981, Reagan and Bush reasoned that leveling with the public that a $50 billion bailout was in the offing would be political suicide. They feared voters would see it as a tax increase—which it was—and thus a breaking of their campaign promises—which it was not, at least not initially. Postponing the inevitable, however, turned a crisis that had not been the fault of either Reagan or Bush into one squarely of their own making. Members of Congress endorsed the White House’s calculus during the decade and were complicit in efforts to deceive. As keeper of the budget, however, the president had an added responsibility to tell the public the truth.

Leaving zombie banks open led to all the market distortions one would expect. By the mid-1980s, the banks’ interest rate squeeze had morphed into a bad-asset situation: problem loans, one created by foolhardy investments—commercial real estate, race horses, brothels, you name it—and too often old-fashioned criminality. That this now would require hundreds of billions of dollars more to fix was the responsibility of Reagan and Bush, albeit with indispensable help from Democrats and Republicans in the legislative branch. Shortly after Bush was sworn in as president in January 1989, he came clean, announcing a massive bailout to close hundreds of hopelessly ill thrifts. But even then, his administration used deceptively low estimates of the cost, saying it was in the neighborhood of $100 billion. Years later, the Government Accountability Office, the watchdog arm of Congress, tabulated the final cost to be $500 billion, almost all borne by taxpayers.

While deposit insurance did not cause the crisis, it enabled politicians to prolong and amplify it. Calming fears to avert runs was the purpose of deposit insurance. It was not meant to calm fears so those seeking power could win elections. Reagan was right to say that government was the problem, but wrong to champion the idea that it’s always so. The indiscriminate distaste for government the Reagan era ushered in was too often misguided by knee-jerk ideology and, in practice, hypocrisy.

Today the Trump White House is returning to the same misguided practice of allowing financial markets to police themselves. Policies embraced by Trump appointees are again exposing consumers to predatory lending, which leads to too much consumer debt and which can cause severe downturns and put federally insured institutions—and taxpayers—at risk. Deposit insurance once again plays the role, as FDR feared it would, of making everyone more confident in the system than is wise.

Only government can do some tasks: provide intellectual property protections, collect taxes, grant bank charters and other incorporations. And only the federal branch can offer meaningful government guarantees such as deposit insurance. (State efforts failed time and again for lack of scale and diversity.) But these functions create an obligation by the government to ensure that those using these benefits do so wisely. That’s the bargain. In the instance of deposit insurance, the bargain FDR struck with its proponents was that, in exchange for bestowing a safety net, government would police those receiving the benefit to make sure they weren’t abusing it. The Reagan White House misunderstood deregulation to be a lifting of the rules and the lifting of oversight when in fact these two facets of regulation need to balance each other. Only government can create and enforce the so-called level playing field of fair rules that robust markets require.

The lesson of the 1980s bank crisis is that FDR was right: without proper safeguards, deposit insurance creates danger. Elected officials should never again be allowed to misuse deposit insurance to further their power.

Kathleen Day spent more than 30 years as a financial reporter, mostly for the Washington Post, before joining the Johns Hopkins Carey Business School in 2013. She continues to contribute to the Post. She is the author of Broken Bargain: Bankers, Bailouts and the Struggle to Tame Wall Street (Yale Univ. Press, 2019). She tweets @kathleenday.

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License. Attribution must provide author name, article title, Perspectives on History, date of publication, and a link to this page. This license applies only to the article, not to text or images used here by permission.