Equifax, Experian, TransUnion: hardly names you’d give the characters in a classic story. And chances are, they’re not names you know much about. But they know about you. Together—as Josh Lauer explains in Creditworthy: A History of Consumer Surveillance and Financial Identity in America (Columbia Univ. Press, 2017)—the nation’s three largest credit bureaus “track the movements, personal histories, and financial behavior of nearly all adult Americans.” So thorough are their methods that personal finance guru Suze Orman believes they should determine not only whether you buy a house, car, or cell phone, but even whom you date. “FICO first,” she suggests (in reference to your prospective partner’s credit score), “then sex.”

Credit cards, which allow consumers to carry interest-generating balances, illustrate what Lauer calls the “monetizing logic of digital capitalism.” Nick Youngson/CC BY SA 3.0

As Lauer put it in a recent interview, Orman’s advice treats creditworthiness as “a category of moral knowledge.” To be determined a good risk is to be judged “honest and industrious.” A poor credit score, on the other hand, reflects not only bad bookkeeping or a modest income but more—a want of “integrity or work ethic.” Lauer’s point here was not about novelty: credit reporting has a long history, one entwined with broader questions of individual worth and virtue, and investigated by such historians as Lendol Calder, Martha Olney, and Louis Hyman. What’s new, he suggested in the interview, is how simultaneously sweeping and opaque consumer data has become, reaching into every corner of our lives while being “coded in ‘objective’ numbers that neutralize the explicit tone of moralizing.”

Rather than commit what Lauer calls “the sin of technological determinism” and treat this development as one more inexorable result of advances in computing, in Creditworthy he treats it historically: as the result of human endeavor (and folly). The book is divided into roughly three sections and begins in the wake of the Revolutionary War, when an informal flow of credit functioned more to circulate wealth than to compromise or diminish it, creating commercial opportunities for Americans with more gumption than capital. Lauer quotes an early 19th-century Austrian immigrant who compared the Old World—where credit was provided only to those with substantial collateral, either land or inherited wealth—to the New, where the practice of extending credit helped chip away at hierarchies rather than fortify them: “In America the case is different. Men there are trusted in proportion to their reputation for honesty and adaption to business. Industry, perseverance, acquaintance with the market, enterprise, in short, every moral qualification of a merchant increases his credit as much as the actual amount of his property.”

A poor credit score reflects not only bad bookkeeping or a modest income but more—a want of “integrity or work ethic.”

Lauer does not use Creditworthy to refute this picture—as boosterish, say, or ideologically blinkered—but to largely confirm it. Early 19th-century loan applicants “with a reputation for hard work and honesty could generally count on receiving credit.” In a marketplace where “trust was a function of familiarity,” lending practices were personal: open to white men who neither “loafed, lied, or repeatedly bungled their affairs.”

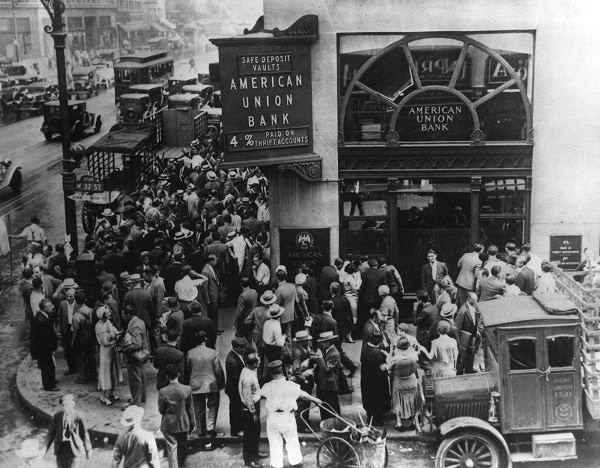

But as the panic of 1837 made plain, early 19th-century demographic changes and economic volatility had altered the contours of the credit market. “As the nation’s population became more numerous and mobile,” Lauer writes, “one was more likely to transact with strangers.” Calculating what risk outsiders posed and successfully collecting on debts gave rise to ever-lengthier inked ledger books then to proprietary credit-scoring algorithms and finally to a national credit infrastructure in which “no digital presence goes untracked, no digital profile goes unmined,” and remaining a stranger takes conscious effort or genuine eccentricity. But it was that early “confounding task of deciding whom to trust and whom to invest in” that led, in fits and starts, “to the development of systematic credit surveillance in the United States.” Louis Hyman—who’s also an editor of the Columbia University Press series to which Creditworthy belongs—reframed this “confounding task” for me in 21st-century terms: “At the center of the recent financial crisis was the simple question: to whom should money be lent?”

How that question was answered—and by whom—occupies Creditworthy’s middle stretch. The data broker industry that is today dominated by a few mammoth firms grew out of “a motley array of private agencies and voluntary protective associations” that compiled “blacklists of debtors and delinquents” based on scattershot data painstakingly collected from municipalities, employers, landlords, banks, merchants, and eventually from utility companies and healthcare providers. During the Progressive Era, the industry was consolidated and its methods made more complex, but its aim remained the same: to “quarantine poor credit risks.” That ambition changed in the 1920s, as credit bureaus began to understand the profit potential of packaging information itself as a commodity and shifted “from an instrument of prevention to one of promotion.”

It is also the moment his villains take the stage, albeit facelessly. Lauer understands the transformation he traces in the book’s first third as a trade-off—one with significant but not perverse or arbitrary costs. In a short piece written for Technology and Culture after the 2008 financial crisis, Lauer made the case that free markets “are never really free” but instead comprise social webs and commercial practices—credit, contracts, and investment decisions among them—that “necessarily ensnare even the politically free in bonds of economic dependency.” Americans live willingly with a “Faustian deal,” having long ago traded their “agrarian self-sufficiency for the heady promises of far-flung interdependence.” Lauer depicts that decision sympathetically: as a compromise with global capitalism but not capitulation.

Less gentle is his treatment of the 20th-century credit bureaus that morphed into ever-larger private firms fixed more on raising revenue than avoiding debt. In Creditworthy’s timeline, that transformation “signaled a major development in the history of American business practice.” As an unnamed president of the Associated Credit Bureaus of America (which led the consumer reporting industry in the 1950s) put it, “credit bureaus were started as a deterrent to putting bad credit on the books.” They had evolved: “Now, credit and credit bureau functions are sales tools.”

A practice once held in low repute—selling customer lists—quietly became the norm, and in an unholy alliance with the postwar advertising industry, banks and credit bureaus developed increasingly sophisticated ways to “monitor the financial performance of consumers and calibrate credit access—expanding or curtailing—to maximize profitability.” Borrowers who failed to pay off loans quickly and in full, once regarded as undesirable credit risks, were now seen as exciting sources of revenue. The ideal loan candidate was no longer an enterprising immigrant who paid small debts back promptly; instead, he was an already overleveraged shopper, susceptible to targeted marketing campaigns and willing to carry “an interest-generating balance without maxing out.”

In the 1920s, credit bureaus began to understand the profit potential of packaging information as a commodity.

When Lauer here refers to ordinary Americans trapped on “the treadmill of debt,” Creditworthy changes course, moving further afield from that optimistic young Austrian and toward the current senior senator from Massachusetts. Elizabeth Warren’s 2014 memoir, A Fighting Chance, catalogs the congressional compromises and court rulings made in the 1980s and ’90s that weakened public protection from predatory banking practices and culminated, she believes, in the 2008 financial crisis. The people Warren interviewed for the Consumer Bankruptcy Project—launched in 1986 to determine the exact factors that led so many citizens onto the road of increasing credit debt and eventual bankruptcy—did not strike her (in Lauer’s memorable phrasing) as loafers, liars, or bunglers. Families who were sometimes homeless, often insolvent, and always “desperately ashamed of their situation” inspired her fight for the federal Consumer Financial Protection Bureau, which Lauer described in the interview as “absolutely essential.” Founded in 2011, the CFPB is now facing a full repeal, and it is worth asking why. Answering that question brings us to the final section of Lauer’s account, which focuses on surveillance, and a further darkening in tone.

However critically he regards methods of mass credit that “trapped Americans in the bondage of debt,” Lauer sounds downright dystopian when describing the ways that system “also ensnared them in bonds of institutional surveillance.” Two congressmen have recently submitted bills to shut down the agency Warren created, working together (as they put it) to sound “the alarm on the CFPB’s federal overreach.” But what Creditworthy makes clear is that citizens have willingly given commercial surveillance systems a breathtaking scope that they would never allow the state. Consider the outrage that greeted Edward Snowden’s National Security Agency leaks revealing the vast reach of the nation’s intelligence-gathering apparatus. Now consider this: in 2012, according to Lauer, “the data broker industry produced $156 billion in revenue . . . more than double what the US government allocated to its own intelligence budget.”

Lauer’s interest in surveillance stems not only from specific concerns about privacy, but from broader questions about what he calls the “monetizing logic of digital capitalism” and a culture that chooses to invest the marketplace with the power to determine the “measure of human value.” Should prompt payments on desirable merchandise be evidence of trustworthiness and sound principles? Suze Orman believes they should. Still, it’s worth asking whether appointing Equifax, Experian, and TransUnion to take the measure of an American’s character surrenders something more elemental than “agrarian self-sufficiency,” a deal with the devil that even Faust might have declined.

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License. Attribution must provide author name, article title, Perspectives on History, date of publication, and a link to this page. This license applies only to the article, not to text or images used here by permission.